Unforeseen circumstances like illnesses and accidents can happen to anyone. Thus, knowing you have something to fall back on can be reassuring. Here’s where health insurance plays an important role to keep you and your family protected. In this article, Annie Wong, Managing Director of Annieway 96 Sdn Bhd, a professional financial planning consultancy, talks about the four types of health policies and how they can benefit us.

When we talk about personal health insurance, there are four different types, each offering various aspects of health-related coverage. If your budget allows it, it is recommended to sign up for all of them to give you full and comprehensive coverage.

Four Types of Health Insurance

- Life Insurance, which will pay out a sum of money to our loved ones if there’s a permanent disability or in the event of death.

- Medical Insurance, which will cover all medical expenses when we are hospitalised, in day-care or undergoing operation or surgery.

- Critical Illness Insurance, which will pay out in cash if we are diagnosed with certain diseases, to ease the burden of our daily living expenses.

- Personal Accident Insurance, which will pay out in cash if we were to lose certain body parts due to an accident.

Each type of insurance plays a role in protecting our income loss or easing the burden of medical expenses. Consider this situation: if a person were to be diagnosed with cancer and require treatment, they might struggle due to the high medical costs. Moreover, most Malaysians depend only on a single-sourced income, and a majority do not have enough savings. When an illness or an accident happens, it would be a tragedy not only for the victims but also for their family members. Health insurance can help mitigate some of these hardships by providing financial assistance in times of need.

How Much Does Health Insurance Cost?

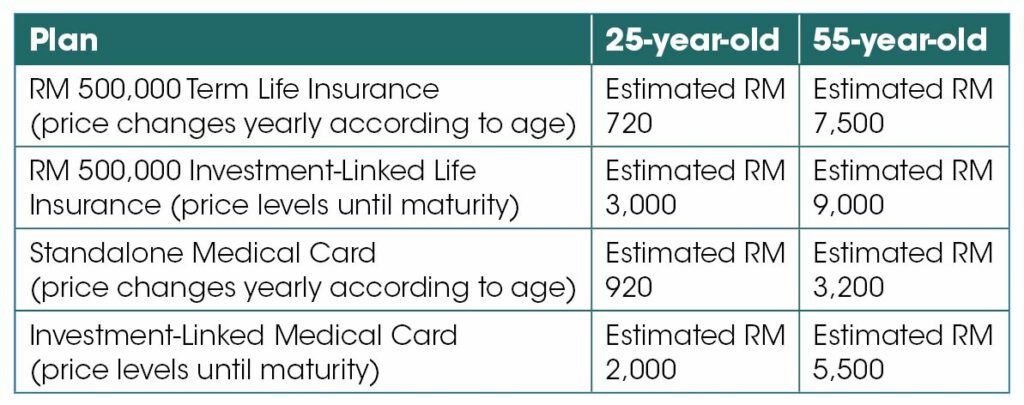

For Life Insurance, Critical Illness, and Medical Insurance, the cost depends on the plan and the insured’s entry age. Here is a simple comparison table to visualise the cost differences between a 25-year-old young man and a 55-year-old senior citizen when purchasing a plan.

- Price estimation is just for illustration purposes. Policies from different companies may vary in pricing.

- Price estimation is based on yearly premiums.

Overall, the cost of Critical Illness Insurance is constantly the highest, followed by Medical Insurance and Life Insurance. The advice here is to purchase insurance as early as possible. This is because when you are young and healthy, you pose a lower risk of facing major medical issues and, therefore, have the opportunity to pay insurance at a lower premium.

Personal accident insurance is determined by the entry age, but the risk level is based on your occupation instead. For example, buying a RM 500,000 personal accident policy would require a 25-year-old logistic driver to pay RM 1,800 while an executive-level 55-year-old man just needs to pay RM 800 as his personal accident policy would be smaller based on his needs.

Many people think that a single medical card is sufficient. Unfortunately, that is not true. The four types of insurance highlighted above are all equally important. Nevertheless, it’s a good idea to talk to a professional financial advisor if you are unsure about what sort of insurance would suit your needs best.